Understanding the Foreclosure Process in San Jose, CA

Introduction

You’re here because foreclosure feels like a looming storm you can’t escape. Maybe you’ve fallen behind on mortgage payments due to unexpected financial challenges, and now you’re overwhelmed by the notices and calls from your lender. You might feel ashamed, uncertain about your rights, or even paralyzed by the complexity of the process. What’s most pressing for you right now is understanding exactly what foreclosure entails, how much time you have, and whether there’s a way to stop it. You’re also likely seeking a way to protect your credit, minimize financial damage, and ideally, keep some equity from your home.

This blog is designed to cut through the noise, offering you clarity about the foreclosure process in San Jose, practical advice to help you regain control, and actionable solutions—like selling your home for cash—that can save you from the worst-case scenario.

Understanding the Foreclosure Process in San Jose, CA

What Is Foreclosure and Why Does It Happen?

Foreclosure happens when homeowners default on their mortgage payments, prompting lenders to initiate a legal process to reclaim and sell the property to recover the owed amount. In San Jose, where housing costs rank among the highest in the nation, this issue is not uncommon. Even one missed payment can trigger a stressful spiral of late fees, mounting debt, and legal notices.

Foreclosure is typically non-judicial in California, which means the lender doesn’t need a court order to sell your home. The process begins with a Notice of Default (NOD) after missing about three months of payments. This notice is a wake-up call, giving you a 90-day period to catch up or resolve the issue. If you’re unable to do so, a Notice of Trustee Sale follows, marking the final steps toward auction and sale.

Financial Toll: Missing payments and foreclosure proceedings come with penalties. Late fees can range from 5-10% of the monthly mortgage, and legal fees might add thousands of dollars to your outstanding balance. For example, on a $3,500 monthly mortgage, just four missed payments could add over $14,000 in fees and arrears.

Emotional Cost: Beyond the dollars, foreclosure impacts your mental health. Anxiety, sleepless nights, and the fear of eviction are common for homeowners navigating this process.

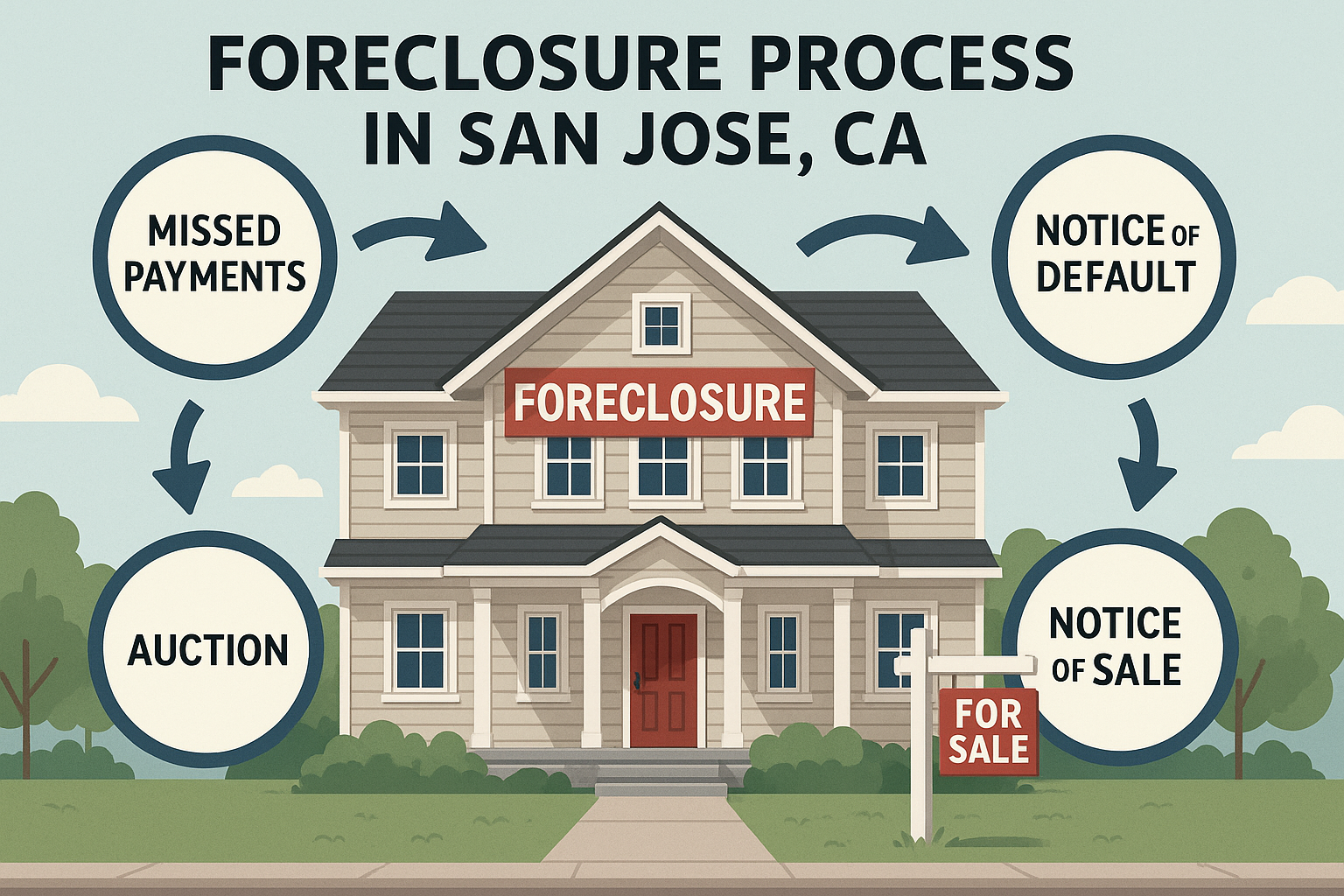

The Key Stages of Foreclosure in San Jose

Stage 1: Missed Payments (Day 1-90)

The foreclosure process unofficially begins with missed mortgage payments. After 30 days, you’ll likely receive a late payment notice, followed by more aggressive communication at 60 and 90 days.

Stage 2: Notice of Default (Day 90)

At this point, your lender files a Notice of Default, a public record indicating you’re officially in foreclosure. You’ll have 90 days to either catch up on payments, negotiate a loan modification, or explore other alternatives.

Stage 3: Notice of Trustee Sale (Day 180)

If you can’t resolve the default, the lender issues a Notice of Trustee Sale, setting an auction date. This is your last chance to act before losing your home.

Stage 4: Auction and Sale (Day 210+)

At auction, your home may be sold to the highest bidder or returned to the lender if no bids are sufficient. At this stage, eviction proceedings might follow if you haven’t vacated the property.

Time Matters: Acting early can save your home or equity. For example, if you explore selling for cash during the Notice of Default period, you can preserve some of your financial stability and avoid the foreclosure stain on your credit.

Learn How To Stop The Bank From Foreclosing On Your California House to explore the most effective strategies to protect your home.

Your Rights as a Homeowner During Foreclosure

California law offers robust protections for homeowners, ensuring lenders follow fair practices. Understanding these rights can empower you during this difficult time.

- Notification and Transparency: Lenders are required to provide a Notice of Default and give you 90 days to address the delinquency.

- Right to Reinstate: Up until five business days before the auction, you have the legal right to pay off the overdue amount—including fees and interest—and reinstate your mortgage.

- Prohibition of Dual Tracking: Under the Homeowner Bill of Rights, lenders cannot proceed with foreclosure while negotiating a loan modification or alternative with you.

- Grace Periods and Forbearance: Depending on your situation, lenders may offer temporary relief, such as reduced payments or a pause in foreclosure proceedings.

Real-Life Example: A San Jose homeowner facing foreclosure managed to reinstate their loan after securing a temporary forbearance agreement. They paid $18,000 in overdue payments and fees just days before the auction.

However, these rights require quick action. Waiting too long limits your options and increases costs.

Alternatives to Foreclosure: What Are Your Options?

If you’re feeling stuck, you’re not alone. Many homeowners don’t realize they have alternatives to foreclosure that can preserve their financial future.

1. Loan Modification

Lenders may agree to modify your loan terms, such as reducing the interest rate or extending the repayment period. While this sounds appealing, approval can be challenging, and the process often takes months.

Cost: Application fees can range from $500 to $1,000, and success isn’t guaranteed.

2. Forbearance Agreements

This temporary relief allows you to pause or reduce payments. However, the missed payments are added to your loan balance, meaning you’ll owe more in the long run.

3. Selling Your Home for Cash

Selling for cash is a fast, straightforward way to avoid foreclosure, protect your credit, and keep some equity. Cash buyers close in as little as 7-14 days and purchase homes as-is, eliminating the need for repairs or upgrades.

Example: A San Jose homeowner facing auction sold their property for $450,000 to a cash buyer. After repaying the $320,000 mortgage and $15,000 in fees, they walked away with $115,000—money they wouldn’t have kept if the home went into foreclosure.

Explore How to Avoid Foreclosure in Santa Clara, CA for more insights on proactive steps you can take.

The Cost of Doing Nothing

Ignoring foreclosure notices only accelerates the process and worsens the financial impact. Foreclosure not only means losing your home but also comes with long-lasting consequences:

- Credit Impact: A foreclosure can drop your credit score by 100-150 points and stay on your record for up to seven years.

- Future Housing Challenges: Renting or buying a new home becomes significantly harder with a foreclosure on your record.

- Loss of Equity: Any equity in your home goes to the lender or is lost entirely during the auction process.

Selling your house for cash isn’t just a way out; it’s a way to protect your financial future.

Conclusion: Act Now to Take Back Control

Facing foreclosure is one of the most stressful experiences a homeowner can endure, but it doesn’t have to end with losing everything. While options like loan modifications or forbearance can provide temporary relief, they’re often time-consuming, uncertain, and may not fully address the root of the problem. Selling your house for cash is a swift and effective way to stop foreclosure in its tracks, protect your credit, and keep any equity you’ve built.

By taking decisive action now, you can avoid the long-term financial and emotional toll of foreclosure. Whether you need to close quickly or want to bypass the hassle of repairs and showings, cash buyers offer a simple, no-nonsense solution. Contact Bay Area Home Offers today to explore how selling your home for cash can help you regain control of your financial future and move forward with confidence.